Best No-Penalty CDs and CD Rates in 2026

Last fact-checked: · Editorial standards

Looking at your savings options right now? If you’re searching for the best no-penalty CDs, you’re in luck; the CD market in 2026 offers genuinely compelling opportunities. The best no-penalty CD rates are currently 4% APY or higher, offering you flexibility to withdraw your money without penalties while earning two and a half times the national average for regular CDs. That’s light years ahead of your standard savings account, and it’s why no-penalty CD rates have become increasingly popular with smart savers who want both security and accessibility.

But here’s what most people miss: not all no-penalty CDs are created equal. The difference between choosing the right no-penalty CD and a traditional certificate of deposit could mean hundreds of dollars in extra earnings or surprising penalties if you don’t understand the rules.

When comparing no-penalty CD rates across different banks, you’ll find variations ranging from 3.75% to 4.30% APY, and those small differences compound significantly over months. Plus, there’s a powerful strategy called CD laddering that can help you earn even more while keeping money accessible through your best no-penalty CDs.

What Is a Certificate of Deposit (CD)?

Before we dive into no-penalty CDs specifically, let’s make sure you understand what a CD actually is. A certificate of deposit is a savings account offered by banks and credit unions where you agree to deposit money for a set period of time (called the “term”) in exchange for a fixed interest rate.

Here’s how it works in practice: You give the bank $5,000, agree to leave it alone for 12 months, and the bank pays you a guaranteed interest rate, say 4.00% APY. At the end of 12 months, you get your $5,000 back plus $200 in interest. No surprises. No market volatility. No daily rate changes.

Key characteristics of traditional CDs:

- Fixed rate: Your interest rate never changes, locked in for the entire term

- Fixed term: Typically 3 months to 5 years (sometimes longer)

- Full FDIC insurance: Up to $250,000 protected by the federal government

- Early withdrawal penalties: If you pull money out before the term ends, you lose some interest (usually 3-12 months’ worth)

- No access during term: Your money is locked away, you can’t touch it without penalty

Think of a traditional CD like a promise you make to the bank: “I promise not to touch this money for 12 months, and in return, you promise to pay me a really good interest rate.” The bank loves that promise because it knows exactly how long it can use your money. They reward that commitment with higher rates than savings accounts offer.

Why CDs matter: The national average interest rate on savings accounts is just 0.05% APY. A regular CD pays 15-30 times more. On $10,000, that’s the difference between earning $5 and earning $400-$500 per year. For conservative savers who don’t want stock market risk, CDs have been a pillar of personal finance for decades.

Current CD rate environment (January 2026): Top CDs are paying 4.00%-4.50% APY depending on term length. That’s significantly higher than the national average (1.61%-1.90%), making CDs genuinely attractive right now.

RELATED How To Save Money For Future in 2026

What Are No-Penalty CDs? The Flexible Alternative

A no-penalty CD (also called a liquid CD or penalty-free CD) works like a traditional certificate of deposit, except with a major twist. You deposit money at a fixed interest rate for a set period, usually 6 to 13 months, but you can withdraw your entire balance anytime without getting hit with early withdrawal penalties.

Think of it as a hybrid between a traditional CD’s high rates and a savings account’s flexibility. You lock in a fixed rate, so it won’t change if the market drops. You get FDIC insurance protection up to $250,000. But you’re not locked in for years, wondering if you made the right choice.

The trade-off? No-penalty CDs pay slightly less than traditional certificates. A traditional one-year CD might hit 4.20% APY, while a one-year no-penalty CD runs closer to 3.95%. That 0.25% difference is the price of flexibility, and for many savers, it’s absolutely worth it.

Best No-Penalty CDs Available Now (January 2026)

These are the actual best no-penalty CD rates you can get today:

Top Performers by Term Length

6-Month No-Penalty CDs:

- Climate First Bank: 4.27% APY, $500 minimum

- What makes it best: Highest rate available in this category, reasonable minimum deposit

9-10 Month No-Penalty CDs:

- Sallie Mae Bank (via Raisin): 4.30% APY, $1 minimum

- Farmers Insurance Federal Credit Union: 4.00% APY, $1,000 minimum

- What makes them best: Sweet spot for rate vs. term length, perfect if you want a shorter commitment

11-13 Month No-Penalty CDs:

- Marcus by Goldman Sachs (11-month): 3.95% APY, $500 minimum

- Marcus by Goldman Sachs (13-month): 3.95% APY, $500 minimum

- Marcus by Goldman Sachs (7-month): 3.90% APY, $500 minimum

- CIT Bank (11-month): 3.75% APY, $1,000 minimum

- Ally Bank (11-month): 3.00% APY, $0 minimum

- What makes them best: Consistent rates, FDIC insurance, multiple term options

Which Bank Should You Choose?

Best Overall: Marcus by Goldman Sachs. Reliable 3.95% rate on multiple terms, $500 minimum, and backed by Goldman Sachs (FDIC insured). Their 5.0 NerdWallet rating reflects consistently strong service.

Best for Maximum Flexibility: Ally Bank. Zero minimum deposit means you can open with just a few dollars. 3.00% APY is lower than competitors’, but the flexibility of no minimum makes it accessible for everyone.

Best for Highest Rate: Sallie Mae Bank via Raisin. 4.30% APY crushes the competition on a 10-month term. Trade-off: Raisin is a platform, so the experience is different than banking directly with a major institution.

Best for Credit Union Members: Farmers Insurance Federal Credit Union. 4.00% APY on 9-month terms with penalty-free early closure each calendar month. If you’re a member, this is worth exploring.

No-Penalty CDs vs. Traditional CDs: Which Should You Choose?

This is the question that matters. Traditional CDs often pay a quarter percent or more above no-penalty alternatives. On $10,000, that’s $25+ per year in extra interest. But here’s the catch: you must keep your money locked away.

Choose a Traditional CD if:

- You’re 100% confident you won’t need this money during the term

- You can commit to longer terms (3+ years) for the highest rates

- You want to maximize every fraction of a percentage point

- Your financial situation is stable with no major changes expected

Choose a No-Penalty CD if:

- You have any uncertainty about future money needs (life changes, job transitions, emergencies)

- You want to lock in today’s rates before they fall

- You value flexibility more than extracting the absolute highest yield

- You might want to move money to higher-rate CDs as rates change

Real scenario: You have $10,000 and see a traditional CD at 4.50% APY versus a no-penalty CD at 4.00% APY. The traditional CD earns $450 in a year; the no-penalty CD earns $400. Difference: $50. But if you need your money 6 months in, the traditional CD penalty could cost $100+. The no-penalty CD? You withdraw penalty-free and keep all $10,200 in earnings.

No-Penalty CDs vs. High-Yield Savings Accounts

This comparison is closer than it used to be. Top high-yield savings accounts now offer rates around 4.20% APY, matching or even beating some no-penalty CDs. So what’s the difference?

Rate certainty.

High-yield savings account rates are variable. When the Federal Reserve eventually cuts rates (and they will), your HYSA rate drops immediately. A 4.20% account becomes 3.20%, and then becomes 2.20% as rates fall. Your no-penalty CD? It stays locked at whatever rate you opened it. That rate protection is significant when rates are falling.

On a $20,000 deposit earning 4.10% in a 1-year CD versus 4.20% HYSA, the CD earns about $820, and the HYSA earns about $840. The HYSA edges out by $20. But that’s only if rates stay stable. If rates fall to 2.50% partway through the year, the HYSA earnings drop to about $360 (a $480 loss compared to your CD).

Access: HYSA wins. You can withdraw anytime. No-penalty CDs require a full balance withdrawal (no partials for most banks).

Bottom line: HYSA if you want complete flexibility and think rates will stay high. No-penalty CD if you want to lock in a rate and don’t need constant access to your money.

Understanding No-Penalty CD Rates: How Much Will You Actually Earn?

Let’s get specific. APY numbers are nice, but real dollars matter more.

| Deposit | 6-Month CD at 4.27% | 11-Month CD at 3.95% | 13-Month CD at 3.95% |

|---|---|---|---|

| $1,000 | $1,021.28 | $1,036.13 | $1,051.29 |

| $5,000 | $5,106.42 | $5,180.63 | $5,256.45 |

| $10,000 | $10,212.84 | $10,361.26 | $10,512.90 |

| $25,000 | $25,532.09 | $25,903.15 | $26,282.25 |

That $25,000 example is worth paying attention to. Over 13 months, you earn $1,282.25 just by parking money in a CD. In a traditional savings account earning 0.05%, that same $25,000 earns $10. The difference is $1,272. That’s real money.

The CD Ladder Strategy: Earning More While Staying Flexible

Here’s where it gets smart. Instead of putting all your money in one CD, a CD ladder spreads it across multiple CDs with different maturity dates. You capture the higher rates of longer-term CDs while keeping cash accessible every few months.

How CD Laddering Works

Let’s say you have $6,000 to invest. Instead of one 13-month CD, you open three CDs:

- $2,000 in a 6-month CD at 4.27% APY

- $2,000 in an 11-month CD at 3.95% APY

- $2,000 in a 13-month CD at 3.95% APY

What happens:

- Month 6: First CD matures. You get $2,000 + interest. You reinvest in a new 13-month CD.

- Month 11: Second CD matures. Reinvest.

- Month 13: Third CD matures. Reinvest.

Now you have regular “rungs” on your ladder where money becomes available. You’re not locked in for years, but you’re earning significantly more than a savings account. Plus, as you reinvest each maturing CD, you capture new rates if they’ve changed.

Why CD Laddering Beats a Single Long-Term CD

A five-year CD might pay 3.85% APY. But rates are falling. If you put all your money in that five-year CD, you’re stuck at 3.85% for five years, even if rates drop to 2.50%. With a ladder, you reinvest portions regularly, adapting to new rates as they change.

Plus, with a ladder, if you face a genuine emergency, some of your money becomes available every 6-12 months without penalty. A five-year CD? You’ll pay significant early withdrawal fees.

How to Choose the Best No-Penalty CD for Your Situation

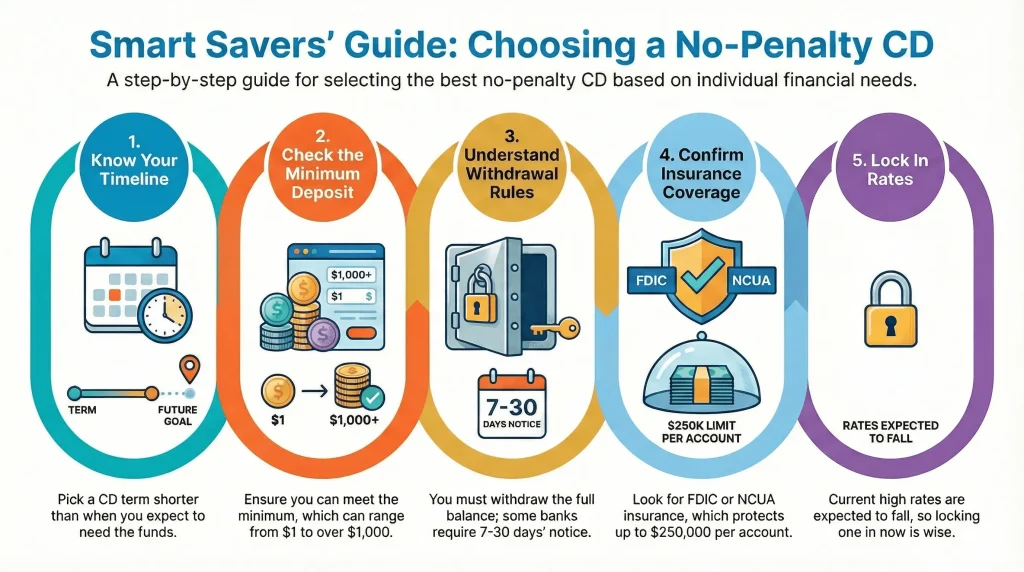

Step 1: Know Your Timeline

When will you need this money? If you might need it in 8 months, don’t lock into a 13-month CD. Pick a 6 or 9-month option. If you’re confident about 12+ months, take the longer rate.

Step 2: Check the Minimum Deposit

Some banks require $1,000 minimums (CIT Bank, Farmers Insurance FCU). Others want just $1 or $500 (Sallie Mae, Marcus). Make sure you can afford the minimum at banks offering the best rates.

Step 3: Understand the Withdrawal Rules

All no-penalty CDs require withdrawal of the full balance (no partial withdrawals). Some require 7-30 days’ notice. Others process instantly online. Check the specific bank’s rules; it matters if you face an emergency.

Step 4: Consider FDIC Insurance

Every bank mentioned here is FDIC-insured up to $250,000 per account. If you have more than $250,000, open accounts at multiple banks to stay fully protected. Credit unions use NCUA insurance (same protection).

Step 5: Lock in Rates Now (Probably)

CD rates are elevated but likely to fall. The Federal Reserve isn’t expected to cut rates dramatically soon, but when it does, CD rates follow quickly. Locking in 4%+ now might look brilliant in 12 months if rates drop to 2.50%.

No-Penalty CD Advantages: Why Savers Love Them

Flexibility Without Penalty: Access your money when life changes, no emergency withdrawals, no surprise fees.

Rate Lock-In: Your rate stays fixed. Even if rates plummet, you keep earning 4.27% or 3.95%, whatever you locked in.

FDIC Insurance: Your money is protected up to $250,000. If the bank fails, you don’t lose a penny.

Predictable Growth: No market volatility. No stock price swings. You know exactly what you’ll earn.

Beat Inflation: At 4%+ APY, you’re outpacing inflation (currently around 2.7%). Your purchasing power actually increases.

Common No-Penalty CD Mistakes to Avoid

Mistake 1: Only checking your current bank’s rates

Your bank might offer 2.91% while Sallie Mae pays 4.30%. That 1.39% difference on $10,000 is $139 annually. Shop around. Online banks consistently beat traditional brick-and-mortar banks.

Mistake 2: Forgetting about auto-renewal

Your CD matures, and if you don’t act, the bank automatically renews it, possibly at a much lower rate. Circle maturity dates on your calendar and shop rates 30 days before maturity.

Mistake 3: Misunderstanding “no-penalty” as “no-cost.”

No-penalty CDs still require full balance withdrawals. You can’t take out half. Some banks require a 7-day notice. Understand the specific terms before opening.

Mistake 4: Choosing the longest term automatically

Longer doesn’t always mean better. A 13-month CD at 3.95% isn’t better than a 6-month at 4.27% if you might need money sooner. Match the term to your actual timeline.

Mistake 5: Ignoring the inflation impact

A 3.75% CD beats a 0.01% savings account, but if inflation is running 2.7%, your real purchasing power gain is only 1.05%. Still better than savings accounts, but know the real return.

No-Penalty CD vs. Traditional CD: Quick Comparison

| Feature | No-Penalty CD | Traditional CD |

|---|---|---|

| Interest Rate | 3.75% – 4.30% | 4.00% – 4.50%+ |

| Early Withdrawal | No penalty, full interest | Penalty (3-12 months interest) |

| Term Length | 6-13 months max | 1 month – 10 years |

| FDIC Insured | Yes, up to $250k | Yes, up to $250k |

| Best For | Uncertain timelines | Locked-in strategies |

Tax Considerations for No-Penalty CDs

CD interest is taxable as ordinary income at your regular tax rate (10-37% depending on brackets). A $20,000 CD earning $800 means you owe taxes on that $800 this year, regardless of when it matures.

The bank will send you a Form 1099-INT if you earn $10+ in interest. Report it on your tax return as interest income. If you withdraw early and pay a penalty, that penalty is tax-deductible.

Tax-smart strategy: Hold CDs in retirement accounts (IRA, 401k) to defer taxes until withdrawal. A CD in a traditional IRA compounds tax-free until retirement.

FAQs: Your No-Penalty CD Questions Answered

Can I withdraw early from a no-penalty CD?

Yes, that’s the whole point. You can withdraw anytime. Most banks require 7 days’ notice, and some process it instantly online. You keep all interest earned up to your withdrawal date. FDIC-insured banks let you withdraw within 7 days of opening with minimal penalties (7 days’ interest max).

How much can I deposit in a no-penalty CD?

Minimums vary by bank and account type. Most range from $1 to $1,000. Maximums are typically unlimited, though FDIC insurance caps protection at $250,000 per bank. You can open multiple CDs at different banks to exceed that.

What happens if I need money before the term ends?

Withdraw it. You’ll get your principal plus all accrued interest with no penalty. Some banks process same-day; others take 3-5 business days. Check the specific bank.

Should I use my emergency fund for a no-penalty CD?

No. Emergency funds should be in checking/savings for instant access. No-penalty CDs are for money you won’t need for 6-13 months. Use them for sinking funds (car repair, home projects, annual expenses), goals that are a few months away, or simply parking cash to beat inflation.

What if rates rise after I open my CD?

You’re locked into your original rate. That’s the trade-off of fixed-rate CDs. However, with no-penalty CDs, you can withdraw and reinvest in higher-rate CDs when rates rise. With traditional CDs, early withdrawal penalties might offset the gain.

Are no-penalty CDs FDIC insured?

Yes. Every no-penalty CD mentioned here is from FDIC-insured banks or NCUA-insured credit unions. Your money is protected up to $250,000 per bank.

Action Plan: How to Open Your First No-Penalty CD

Step 1: Decide Your Amount and Timeline (Today)

How much can you invest? When might you need it? These two answers determine which CD works.

Step 2: Compare Rates Across Banks (15 minutes)

Visit NerdWallet, Bankrate, and Investopedia’s CD comparison tools. Check the banks recommended here directly. Write down the top 3 options with their rates, minimums, and terms.

Step 3: Open the Account (10-15 minutes)

Most banks let you apply online. You’ll need ID, Social Security number, and a linked bank account for funding. Many offer same-day or next-day account opening.

Step 4: Fund Your CD (1-3 business days)

Transfer money from your checking account. Some banks let you fund immediately; others take a few days to clear funds.

Step 5: Set a Calendar Reminder (1 minute)

30 days before maturity, get a notification. At that point, shop rates again. Decide: reinvest in a new CD, switch banks, or withdraw and move money elsewhere.

Step 6: Avoid Auto-Renewal (At maturity)

If you don’t act, most banks auto-renew at current rates, which could be much lower. Don’t let that happen. Actively choose your next move.

The Bottom Line: Best No-Penalty CDs for 2026

No-penalty CDs offer a genuine middle ground in today’s rate environment. You get 4%+ yields without locking your money away for years. That’s two and a half times the national average. Not bad for a low-risk account.

Right now, Sallie Mae Bank (4.30% APY) and Climate First Bank (4.27% APY) lead on rates. Marcus by Goldman Sachs offers consistency across multiple terms with strong backing. Ally Bank removes barriers with zero minimums.

The strategy matters as much as the bank. CD laddering solves the classic problem: higher rates come with long terms you might not want. A ladder gives you higher earnings with quarterly access points.

The real question isn’t which CD is best; it’s which fits your timeline and risk tolerance. If you’re uncertain about future money needs, no-penalty CDs are the answer. If you’re certain about locking money away for years, traditional CDs squeeze out slightly higher rates.

Rates won’t stay this high forever. The Federal Reserve doesn’t cut immediately, but when they do, CD rates follow. Locking in 4%+ today might look brilliant in 12 months.

Start shopping today. The difference between 3.75% and 4.30% on $25,000 is $137.50 per year. That’s not huge, but it’s your money. Might as well earn the highest rate available.

Sarah Whitman is the Lead Editor at Keenpocket, where she oversees content standards and reviews every published article for accuracy and clarity. With over six years of experience writing about personal finance, Sarah focuses on practical money advice that works for everyday people — covering budgeting, saving strategies, side hustles, debt management, and beginner investing. She believes good financial advice should be honest, actionable, and useful in real life, not just textbook scenarios.