How to Refinance Student Loans in 2026

Last fact-checked: · Editorial standards

Wondering how to refinance student loans? Learn how to lower your interest rate, reduce monthly payments, and pay off debt faster. Understand the process, key advantages, and what to watch out for before you decide.

Student loan refinancing swaps out your current loans for a new private loan with different terms. Refinancing with a private lender might lower your interest rate, reduce your monthly payment, or change your repayment timeline.

This works for both federal and private student loans, but you’ll need to meet certain credit and income standards.

Many folks look into refinancing to save on interest or just to combine several loan payments into one. You’ll need decent credit and a steady income — though some lenders let you use a co-signer if you’re not quite there yet.

Your decision depends on your current loan terms, your finances, and what you want for the future.

If you understand how refinancing works, you can make better choices about your money. You’ll want to know how to compare lenders, what documents to gather, and how refinancing might affect your loan benefits.

This guide lays out the main factors that affect your rates and walks you through managing your new loan after it’s approved.

Understanding How to Refinance Student Loans

Student loan refinancing means you replace your current loans with a new private loan, usually with a different interest rate. This isn’t the same as federal consolidation, and there are some trade-offs you need to know about.

What Is Student Loan Refinancing

Refinancing just means you take out a new private loan to pay off your old student loans. The private lender gives you a new loan with its own terms.

You’ll make payments to the new lender instead of juggling different servicers.

Key features of refinancing:

- New interest rate (fixed or variable)

- New repayment term (usually 5-20 years)

- New monthly payment amount

- Just one loan servicer

You can refinance federal loans, private loans, or both at once. But the new loan will always be private — even if you refinance federal loans.

Private lenders look at your credit score, income, and debt-to-income ratio when setting your rate. Stronger financials usually mean lower rates.

How Refinancing Differs from Consolidation

Refinancing and consolidation aren’t the same thing, and they lead to different results.

Federal Direct Consolidation combines your federal loans into one new federal loan. The interest rate is just the weighted average of your old rates, rounded up a bit.

You keep all your federal benefits, like income-driven repayment plans and forgiveness programs. There’s no credit check involved.

Student Loan Refinancing gives you a private loan from a private lender. Your rate depends on your credit and what’s happening in the market.

Refinancing federal loans makes you lose all federal benefits. Private lenders check your credit and income.

| Federal Consolidation | Private Refinancing |

|---|---|

| Keeps federal benefits | Loses federal benefits |

| Weighted average rate | Market-based rate |

| No credit check | Requires credit check |

| Only federal loans | Federal and private loans |

Benefits and Drawbacks

Benefits of refinancing:

- Lower interest rates if you qualify

- One simple payment each month

- Choice of repayment length

- Possible lower monthly payments

Drawbacks of refinancing:

- You lose federal loan benefits

- No more income-driven repayment plans

- No loan forgiveness options

- Variable rates can rise

Federal benefits you lose include:

- Public Service Loan Forgiveness

- Income-driven repayment plans

- Federal forbearance and deferment

- Future federal loan forgiveness programs

Refinancing usually makes sense if you’ve got good credit, stable income, and don’t need federal protections. If you work in public service or struggle to make payments, it’s probably not the move.

Private loans don’t offer federal perks, so refinancing those can make more sense. You might get a better rate or terms without giving up important protections.

When to Consider Refinancing Student Loans

The best time to refinance depends on your credit, income, and the details of your loans. You’ll need to meet certain requirements and have the right kind of loans.

Best Times to Refinance

You might want to refinance if your credit score has gone up since you first borrowed. A higher score can snag you a better interest rate.

Credit Score Improvements

- Score jumped by 50+ points

- No missed payments in the last year

- Lower debt-to-income ratio

If your income has grown, that helps too. Lenders like borrowers with steady, higher paychecks.

Income Changes

- Got a raise or promotion

- Landed a higher-paying job

- Added a cosigner with solid credit

It’s also smart to refinance if market rates drop below your current rate. That’s just money saved.

If you want to remove a cosigner from your original loan, refinancing does the trick.

Loan Types Eligible for Refinancing

Most student loans qualify for refinancing, but the rules vary by type.

Federal Student Loans

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- PLUS Loans

- Stafford Loans

Private Student Loans

- Bank loans

- Credit union loans

- Online lender loans

If you refinance federal loans, you lose federal perks like income-driven repayment and forgiveness options.

Lost Federal Benefits:

- Public Service Loan Forgiveness

- Income-Based Repayment plans

- Deferment and forbearance

- Death and disability discharge

Private loans don’t come with those benefits, so you’re not giving up as much by refinancing them.

Eligibility Criteria

Lenders set clear requirements for refinancing student loans.

Credit Score Requirements

Most want to see a credit score of 650 or higher. For the best rates, you might need 700+.

Income Requirements

You’ll need a steady income. Lenders ask for proof of employment and want to see that you can cover your monthly expenses and loan payments.

Debt-to-Income Ratio

Your total monthly debt payments should be less than 36-43% of your income.

Other Requirements:

- U.S. citizenship or permanent residency

- Graduated from an eligible school

- No recent bankruptcies

- Minimum loan amount (usually $5,000-$10,000)

If you fall short, adding a cosigner can help you qualify.

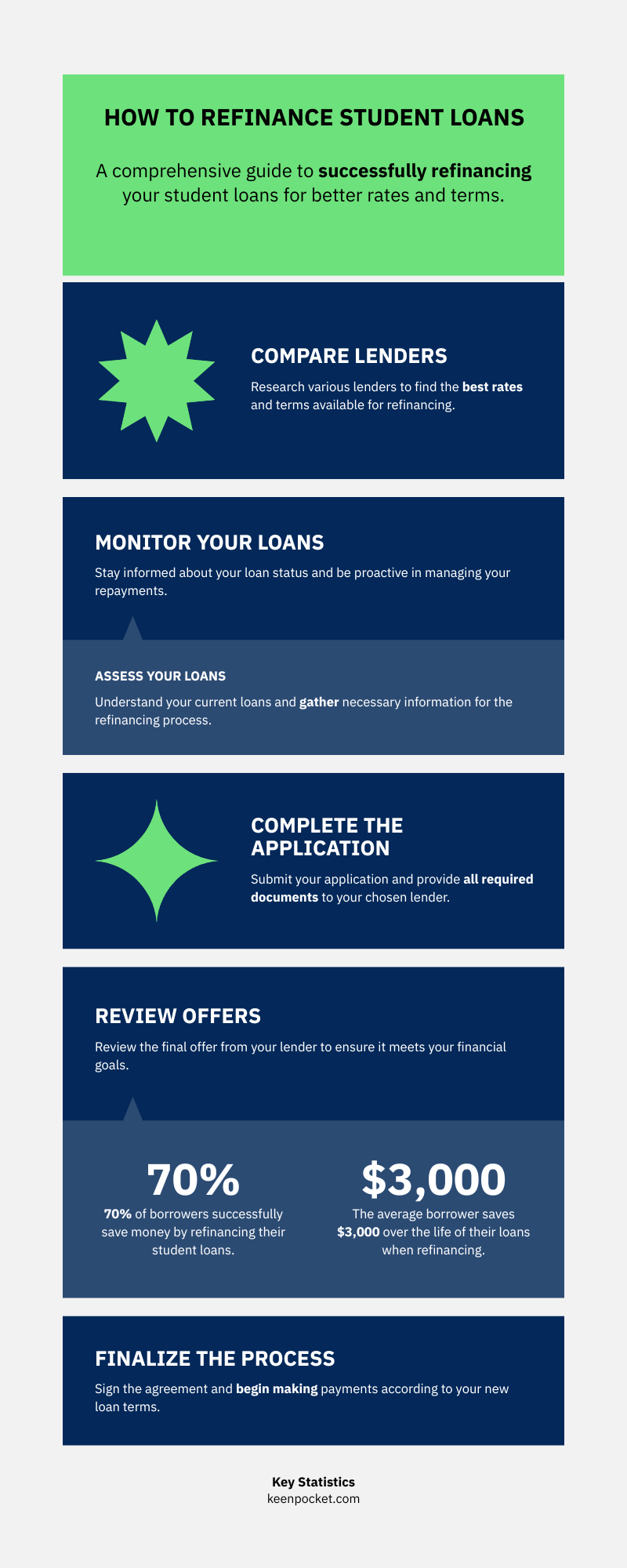

Steps to Refinance Student Loans

The process starts by checking if you qualify and could save money, then comparing rates from different lenders, and finally applying with the right documents.

Evaluate Your Financial Situation

Check your current loan details. Write down your interest rates, monthly payments, and remaining balances for each loan.

Pull your credit score. Most lenders want at least 650 for a decent rate. You can usually check your score for free through your bank or credit card account.

Figure out your debt-to-income ratio. Add up all your monthly debt payments and divide by your monthly income. Lenders usually want this below 40%.

Review your employment and income. You’ll need a steady income, so grab recent pay stubs or tax returns to show proof.

If you have federal loans with special benefits, think hard. Refinancing federal loans with a private lender means you lose income-driven repayment, forgiveness, or deferment options.

Compare Lenders and Loan Offers

Research at least three to five lenders. Banks, credit unions, and online lenders all have different offers.

Pay close attention to interest rates. Look at both fixed and variable rates. Fixed rates stay put, but variable ones can change.

Compare things like:

- Loan terms: 5, 10, 15, or 20 years

- Fees: Application, origination, or prepayment fees

- Repayment options: Autopay discounts, hardship help

- Customer service: Online tools and support

Get rate quotes from a few lenders. Most let you check rates with a soft credit pull, so it won’t ding your score.

Run the numbers on total interest costs for each offer. Sometimes a lower monthly payment means you pay more in the long run.

Application and Documentation Process

Apply online or by phone with your chosen lender. The application usually takes 15-30 minutes.

Have these documents handy:

- Driver’s license or state ID

- Social Security card

- Recent pay stubs (2-3 months)

- Tax returns (last 2 years)

- Bank statements

- Current loan statements

- Proof you graduated

Submit your application and wait for a decision. Lenders usually get back to you in 2-15 business days.

Read the loan terms carefully before you sign. Make sure the interest rate, monthly payment, and repayment timeline match what you expected.

Your new lender pays off your old loans directly. This part can take 2-6 weeks. Keep making payments on your current loans until you know they’re paid off.

Factors That Affect Student Loan Refinance Rates

Your interest rate mostly depends on three things: your credit score shows how trustworthy you are, your debt-to-income ratio tells lenders how much debt you can handle, and your job and income show that you can pay the loan back.

Credit Score Impact

Your credit score is the biggest factor for refinance rates. Most lenders want 650 or above to approve you.

Credit Score Ranges:

- 740+: Best rates out there

- 680-739: Good rates

- 650-679: Average rates

- Below 650: You’ll probably need a cosigner

Lenders use your score to decide if you’ll pay back the loan. A higher score means you pay bills on time and manage debt well.

If your score’s improved since you first got your student loans, you could get a lower rate now. Maybe you’ve built credit history or paid off other debts.

You can check your credit score for free with your bank or credit card company. If your score’s low, give it a few months — paying bills on time really helps.

Debt-to-Income Ratio

Your debt-to-income ratio measures how much of your monthly income goes toward debt. Lenders usually want this ratio to be 50% or less for the best rates.

How to Calculate:

- Add up all your monthly debt payments.

- Divide that total by your gross monthly income.

- Multiply by 100 to get the percentage.

If you pay $1,500 each month toward debt and earn $4,000, your ratio comes out to 37.5%. That’s a solid number and usually gets you better rates.

Lenders like lower ratios because they show you can handle your current debts and add a new loan. If your ratio is up there, try paying down credit cards or other debts before you apply.

Type of Employment and Income

Lenders really prefer borrowers with stable jobs and steady paychecks. Your employment type can affect both your rate and your odds of getting approved.

Best Employment Types:

- Full-time, permanent jobs

- Government positions

- Stable industries like healthcare or education

Contract workers, freelancers, and part-timers usually see higher rates. Lenders see these jobs as riskier, so they bump up the interest to cover themselves.

Your income matters too. Higher earners tend to snag lower rates since lenders figure you can handle the payments more easily.

Most lenders want at least two years of work in your current job or field. If you just started somewhere new, it might be worth waiting until you’ve built more history.

Choosing the Right Student Loan Refinance Lender

Finding the right refinance lender means weighing interest rates, loan terms, and the company’s reputation. The best lenders offer good rates and get positive feedback from customers.

Reviewing Interest Rates and Terms

Interest rates matter most when you pick a refinance lender. Always compare rates from at least three to five companies.

Check out both fixed and variable rate options. Fixed rates stay the same for the life of your loan. Variable rates can jump around — sometimes for the better, sometimes not.

Key terms to compare:

- Interest rates (APR)

- Loan repayment periods

- Monthly payment amounts

- Origination fees

- Prepayment penalties

See if you qualify for any rate discounts. Many lenders shave off a bit if you set up autopay, or if you’re already a customer.

Your credit score plays a big role in the rates you get. If your score has gone up since your original loans, you might qualify for something better.

Check rates from a few lenders before you pick one. Most let you see your rates without dinging your credit score.

Lender Reputation and Reviews

Dig into each lender’s customer service before you apply. Read reviews from real people on independent sites.

Check their Better Business Bureau rating. Watch for complaints about payment processing or customer service headaches.

Important factors to research:

- Customer service hours

- Online account tools

- Payment processing reliability

- Response time for questions

- Complaint resolution history

Ask about forbearance and deferment options. Good lenders help out if you hit a rough patch financially.

Find out who will actually service your loan. Some lenders keep it in-house; others hand it off to a third party.

Some lenders toss in extras like career coaching, financial planning tools, or even unemployment protection. Worth asking about, honestly.

Potential Risks and Considerations

Refinancing student loans can backfire if you don’t know what you’re giving up. Federal loan benefits disappear for good, and some lenders tack on fees that eat up your savings.

Loss of Federal Loan Protections

Refinancing federal student loans with a private lender means you lose all federal protections. There’s no going back after you do it.

Income-driven repayment plans aren’t available after refinancing. Those plans cap your payments at 10-20% of your income, and sometimes even drop payments to $0 if your income falls.

Federal loan forgiveness programs vanish completely. You lose access to:

- Public Service Loan Forgiveness (PSLF)

- Teacher Loan Forgiveness

- Income-driven repayment forgiveness after 20-25 years

Deferment and forbearance get much more limited. Federal loans offer automatic deferment for things like unemployment or going back to school. Private lenders set stricter rules and shorter time frames.

Death and disability discharge protections may not exist with private loans. Federal loans get forgiven if you die or become totally disabled.

Prepayment Penalties and Fees

Most student loan refinancing doesn’t come with prepayment penalties, but always double-check your loan agreement. Some lenders sneak in fees that can shrink your savings.

Application and origination fees can run 1-5% of your loan. For a $50,000 loan, a 2% fee means $1,000 tacked on right away.

Late payment fees are all over the map. Some charge a flat $25, others hit you with a percentage that can reach $100 or more.

Check processing fees show up if you pay by check instead of autopay. Usually $5-15 per payment, which adds up.

Read every loan document before you sign. Make sure the fees don’t wipe out your interest savings over the loan term.

Impact of Refinancing on Federal Loan Benefits

Refinancing federal student loans with a private lender means you give up all federal protections and programs. Once you finish the process, there’s no way to reverse it.

Forbearance and Deferment Changes

Federal loans offer forbearance and deferment to pause payments during tough times. You can request forbearance for up to 12 months for things like unemployment or medical issues.

Deferment covers specific situations — going back to school, military service, or economic hardship. With subsidized loans, interest might not pile up during deferment.

Private lenders have their own rules for pausing payments. Some offer short-term forbearance, others don’t offer much relief at all.

Your options get limited after refinancing. Private lenders usually expect you to keep paying, even during financial stress. That safety net from federal loans? Gone.

Public Service Loan Forgiveness Implications

Public Service Loan Forgiveness (PSLF) wipes out your remaining federal loan balance after 120 qualifying payments. You need to work full-time at a government or nonprofit job.

Only federal Direct Loans count for PSLF. Once you refinance, your loans are private, and PSLF is off the table. There’s no way to switch back.

Income-driven repayment plans also disappear if you refinance. These plans cap your payment based on income and can lead to forgiveness after 20-25 years.

If you’re working in public service or hoping for loan forgiveness, it’s usually smarter to keep your federal loans. The savings from refinancing often don’t make up for losing those programs.

Improving Approval Odds for Student Loan Refinancing

Your approval for student loan refinancing rides on your credit score and debt-to-income ratio. A credit score of 650 or higher gives you the best shot with most lenders.

Boosting Your Credit Score

Lenders check your credit score first. Most want to see at least 650. Anything lower makes approval much tougher.

Check your credit report first. Look for mistakes like wrong payment dates or accounts that aren’t yours. Dispute anything with the credit bureaus.

Pay down credit card balances. Keep your credit utilization under 30%, or even better, under 10% for top scores.

Pay on time — every time. Payment history makes up 35% of your score. Set up autopay so you don’t miss a due date.

Don’t close old credit cards. Leave your oldest accounts open to keep your credit history long. That average account age helps.

Hold off on new credit applications. Each hard inquiry dings your score a bit. Wait until after you refinance to apply for anything new.

Lowering Your Debt-to-Income Ratio

Lenders want to see that your debt payments don’t eat up too much of your income. Most want a debt-to-income ratio under 40%.

Calculate your ratio. Add up all your monthly debt payments and divide by your gross monthly income. Include credit cards, car loans, and your student loans.

Increase your income. Take extra shifts, freelance, or grab a part-time gig. Even a short-term boost can help.

Pay down other debts. Knock out high-interest credit cards first. Every debt you clear drops your ratio.

Think about a cosigner. If your ratios are still high, a cosigner with solid credit and income can boost your approval odds. Just know they become responsible if you can’t pay.

Key Documents Needed for Student Loan Refinancing

Lenders usually ask for similar documents to process your application. You’ll need to show proof of income, details about your current loans, and ID.

Proof of Income

Lenders want to know you can handle the new loan payments. Your income documents show you’ve got steady money coming in.

Recent pay stubs are the go-to. Most lenders want your last two or three. These should show your gross income and any deductions.

Tax returns from the past year or two paint a bigger picture. Self-employed folks usually need these. W-2 forms work if you’re on payroll.

Bank statements from the last couple of months show your cash flow. Some lenders check that your deposits match what you claim.

If you’re out of work or between jobs, you might need a cosigner with a steady income. The cosigner’s documents get added to your application.

Loan Statements

You need up-to-date info on all the loans you want to refinance. Lenders use this to total your debt and set up payoffs.

Current loan balances show what you owe. Grab recent statements from each loan servicer — nothing older than 30 days.

Interest rates on your current loans help you compare offers. Your statements should list both fixed and variable rates.

Loan servicer contact info speeds up payoffs. Write down phone numbers and account numbers for each loan. Some lenders handle payoffs directly with your servicers.

Payment history might be needed by some lenders. Good records can help you get a better rate.

Identification Requirements

Lenders need to verify who you are before approving you. Keep these documents handy, especially for online applications.

Your Social Security number goes on all applications. You’ll probably enter it a few times.

A driver’s license or state ID serves as your photo ID. Most lenders accept digital photos or scans.

Proof of address shows where you live. Utility bills, lease agreements, or bank statements all work. Make sure it’s recent and lists your current address.

Your date of birth gets checked against official records. This helps prevent identity theft and keeps credit checks accurate.

Managing Your New Student Loan After Refinancing

After you finish refinancing, you’ll need to set up new payment systems and keep an eye on your new loan. Your loan servicer and payment setup will probably look different than before.

Setting Up Repayment Options

Reach out to your new lender during the first week. Let them know your preferred way to pay.

Most lenders offer automatic payments, and honestly, that’s usually the easiest. Plus, you might snag a 0.25% interest rate discount for setting it up.

Go ahead and set up your online account access right away. You’ll need it to check statements, make payments, or fix your contact info if you move or change your email.

Payment Options Available:

- Automatic bank transfer (most folks go with this)

- Online manual payments

- Phone payments (sometimes there’s a fee — why do they do that?)

- Mailed checks (definitely the slowest)

Pick a payment date that fits your income schedule. Usually, lenders let you choose any date from the 1st to the 28th.

If you can swing it, try bi-weekly payments instead of monthly. It could help you pay off your loan a bit faster and cut down on interest.

Don’t forget to tweak your budget for your new payment amount. Double-check if your monthly payment changed compared to your old loans.

Monitoring Account and Payments

Take a few minutes each month to check your account and make sure your payments went through. If something’s off, it could hurt your credit score, and that’s no fun to fix later.

Glance over your loan statements for surprises, like interest rate hikes or changes to your terms. If you’ve got a variable rate loan, it might shift when you least expect it.

Key Items to Monitor:

- Payment due dates

- Current balance

- Interest rate changes

- Contact information updates

- Tax documents (1098-E forms)

Set up account alerts so you don’t miss payments or updates. Most lenders will text or email you if you ask — might as well use that.

Hang on to records of your payments and any messages from your lender. Honestly, just save them on your computer or in the cloud for easy access.

Use online calculators or your lender’s website to track how close you are to paying off your loan. It’s actually motivating to watch the balance drop, and you can plan for an early payoff if you’re feeling ambitious.

Please Like and Follow Our Facebook Page

Sarah Whitman is the Lead Editor at Keenpocket, where she oversees content standards and reviews every published article for accuracy and clarity. With over six years of experience writing about personal finance, Sarah focuses on practical money advice that works for everyday people — covering budgeting, saving strategies, side hustles, debt management, and beginner investing. She believes good financial advice should be honest, actionable, and useful in real life, not just textbook scenarios.