Debt Snowball Method: How to Pay Off Debt Fast in 2026 (Free Printable Tracker)

Last fact-checked: · Editorial standards

You make payments every single month. The balances barely move. One card here, a car loan there, that medical bill you keep pushing to next month. It feels like you’re pouring water into a bucket with a hole in the bottom.

Here’s the thing nobody tells you: most people don’t fail at paying off debt because of math. They fail because of motivation. Three months in, nothing feels different, so they quit.

The debt snowball method fixes the motivation problem first. You pay off your smallest debt before anything else, no matter the interest rate. That first win comes fast, sometimes within a month or two. Then you roll that payment into the next debt, and the next, until the “snowball” is big enough to crush your largest balance.

In this guide, you’ll learn exactly how to set up your snowball in four steps, how to find extra money to feed it, how it compares to the avalanche method, and how to use a printable tracker to keep yourself going when progress feels slow. You’ll also see a real example with real numbers, so you know what to expect month by month.

People who follow this method consistently become debt-free in 18 to 36 months on average. Not overnight. But faster than you think, and for good.

Let’s build your snowball.

Quick Answer

The debt snowball method works like this: list all your debts from smallest balance to largest, ignoring interest rates. Pay the minimum on everything except the smallest debt. Throw every spare dollar at that smallest debt until it’s gone. Then add its payment to the minimum of the next-smallest debt and repeat. Each payoff frees up more money, so your payments “snowball” larger with every debt you eliminate. Quick early wins keep you motivated to finish.

What Is the Debt Snowball Method (in Plain English)?

The debt snowball method is a debt payoff strategy where you attack your debts in order of balance size, smallest first. Interest rates don’t decide the order. Balance size does. If you owe $400 on a store card, $2,100 on a credit card, and $9,500 on a car loan, the $400 store card goes first, even if it has the lowest rate.

It works because of the way human brains handle long-term goals. A study in the Harvard Business Review found that people who paid off small balances first were more likely to eliminate their debt than those who spread payments out. Each closed account is proof that the plan works. Proof keeps you going. Spreadsheet-perfect math doesn’t help if you abandon the plan in month four.

The method is best for people with three or more debts who have struggled to stay consistent before. If you have just one debt, you don’t need a snowball. And if you’re someone who genuinely stays disciplined for years without needing wins, the avalanche method may save you more in interest. We’ll compare both later in this guide.

Why Paying the Smallest Debt First Actually Works

Quick wins rewire how you feel about your money. When you close that first account, even a tiny one, something shifts. Debt stops being this fog hanging over your life and becomes a list you’re actively shrinking. That emotional shift is the entire engine of the snowball. You’re not just paying debt. You’re winning, visibly, on paper, every few months.

There’s a practical benefit too. Every debt you close removes a minimum payment from your monthly obligations. Fewer bills means fewer due dates to track, fewer chances for a late fee, and more breathing room if your income hiccups. Someone juggling seven minimum payments is one missed paycheck away from chaos. Someone with two payments has options.

The honest caveat: the snowball usually costs more in total interest than paying high-rate debts first. For most people, the difference is a few hundred dollars spread over two or three years. That’s the price of a plan you’ll actually finish. A mathematically perfect plan you quit is worth nothing.

Not sure how much extra you can put toward debt each month? Start with the 50/30/20 budget rule to see exactly where your money goes.

Step 1: List Every Debt From Smallest to Largest

Get every debt out of your head and onto one page. Log into each account and write down four things: the name of the debt, the current balance, the minimum payment, and the due date. Include credit cards, store cards, car loans, personal loans, medical bills, money owed to family, and old collections. Leave your mortgage out. The snowball is for consumer debt.

Now sort the list by balance, smallest at the top. Ignore interest rates completely while you do this. A $300 medical bill at 0% goes above a $4,000 card at 24%. That feels wrong if you’re math-minded, but the order is the whole point of the method.

Expect this step to sting a little. Most people have never seen their total debt as one number, and the total is usually bigger than they guessed. Write it down anyway. That number is your starting line, and you’ll never have to see it this big again. Pull a free credit report at AnnualCreditReport.com to catch any debts you’ve forgotten about.

Step 2: Pay Minimums on Everything Except the Smallest

Every debt on your list except the one at the top gets exactly its minimum payment. Not a dollar more. This feels uncomfortable, especially toward a big card that’s racking up interest, but it’s deliberate. Spreading extra money across five debts means none of them die. Concentrating on it means one dies fast.

Set every minimum payment to autopay right now, today, while you’re thinking about it. Autopay protects the plan. One late payment can mean a $30 fee and a penalty interest rate, which is your snowball rolling backward. With minimums automated, you only have one active decision each month: how much extra goes to the target debt.

One important exception before you start: keep a small starter emergency fund of $500 to $1,000 in savings first. Without that cushion, the first car repair or dental bill lands on a credit card, and you’ll undo a month of progress in one swipe.

A starter cushion of $500 to $1,000 is enough to begin, but if you want to calculate your exact number, here’s how much emergency fund you actually need.

Step 3: Attack the Smallest Debt With Everything You Have

This is where the snowball gets fun. Take every spare dollar you can find each month and send it to the smallest debt on top of its minimum. If your budget frees up $150 extra and the minimum is $25, that debt receives $175 a month. A $400 balance is gone in under three months at that pace.

Make the extra payment the day after payday, not at the end of the month. Money that sits in a checking account gets spent. People who pay their snowball first, like a bill, send two to three times more toward debt than people who send “whatever’s left over.” There is never anything left over. You have to take it off the top.

Round up when you can. If you owe $312, scrape together $312 and end it this month instead of dragging $12 into the next. Closing the account is the win you’re chasing, and the sooner it happens, the sooner the method proves itself to the most important skeptic: you.

Step 4: Roll the Payment Into the Next Debt (the Snowball Effect)

When debt one dies, take its entire payment, the minimum plus all the extras, and add it to the minimum of debt two. Nothing goes back into your lifestyle. If you were sending $175 to the store card and debt two has a $60 minimum, debt two now gets $235 a month. When that one dies, debt three gets $235 plus its own minimum. The payment grows like a snowball rolling downhill, which is where the name comes from.

This is the step where the math turns in your favor. Your biggest debt, the scary one, will eventually face the largest monthly payment you’ve ever made, built entirely from payments you were already making. A $9,500 car loan that once felt permanent gets hit with $500 or $600 a month and folds in under two years.

Write the new payment amount on your tracker the same day you close each account. Watching that number climb from $175 to $235 to $410 is the single most motivating part of the whole process.

Curious what your budget looks like once that first minimum payment disappears? Run your new numbers through our free budget calculator and watch the breathing room appear.

How to Find Extra Money to Feed Your Snowball

Your snowball is only as strong as the extra money behind it, and most budgets hide more than you’d expect. Start with the big three: subscriptions, food, and insurance. Cancel anything you haven’t used in 30 days, plan five dinners a week before you shop, and get two fresh quotes on car insurance. Those three moves alone free up $100 to $300 a month for a typical household, with no real drop in quality of life.

Then look at the income side, because cutting has a floor, but earnings don’t. Selling unused stuff around the house is the fastest start. Most homes have $500 to $1,000 worth of forgotten electronics, furniture, and clothes. After that, even one focused weekend gig a month, like delivering food or watching a neighbor’s pets, can add $200 or more directly to the target debt.

Mark every windfall for the snowball before it hits your account: tax refunds, work bonuses, birthday cash, that third paycheck in a two-paycheck budget month. Windfalls are how people shave six months off their payoff date without changing daily spending at all.

Need bigger fuel than coupon-level savings? These side hustles to make extra money can add a few hundred dollars a month straight to your target debt.

Debt Snowball vs Debt Avalanche: Which One Should You Pick?

The avalanche method is the snowball’s rival. Instead of the smallest balance first, you pay the highest interest rate first. On paper, Avalanche always wins or ties. Targeting a 27% card before a 6% loan means less interest paid overall and sometimes a slightly faster finish.

So why does this guide teach the snowball? Because the gap is smaller than people think, and the quit rate matters more. On a typical $20,000 debt load, the avalanche might save $300 to $700 in interest over two or three years versus the snowball. But research on real borrowers keeps finding the same pattern: people using small-wins approaches stick with the plan at higher rates. Saving $500 in theory means nothing if you abandon ship in month five.

Pick the avalanche if your highest-rate debt is also close to your smallest, if the rate gap between your debts is huge (think 29% versus 4%), or if you know from experience that you don’t need motivational wins. Pick the snowball if you’ve started and quit before. A hybrid works too: snowball order, but bump any debt above 25% interest to the front.

A Real Example: $13,000 Paid Off Month by Month

Numbers make this concrete. Meet a sample budget with four debts: a $400 store card ($25 minimum), a $1,800 medical bill ($50 minimum), a $3,300 credit card ($90 minimum), and a $7,500 car loan ($260 minimum). Total: $13,000 in debt and $425 in minimums. After trimming the budget, there’s $250 extra each month.

Months one through two: the store card gets $275 a month ($25 minimum plus $250 extra) and dies in six weeks. Months two through eight: the medical bill gets $325 a month and disappears. Months eight through sixteen: the credit card faces $415 a month, gone before month seventeen. Then the car loan takes the full force: $675 a month. The loan that had years left on paper collapses in about ten more months.

Total time: roughly 26 months from first payment to debt freedom, and the final year runs almost on autopilot. The same person spreading $250 evenly across four debts would still be juggling all four well past the two-year mark, with no closed accounts to show for it.

Once your snowball ends, redirect that final payment into savings. Here’s how to save your first $1,000 in 90 days using the exact same focus.

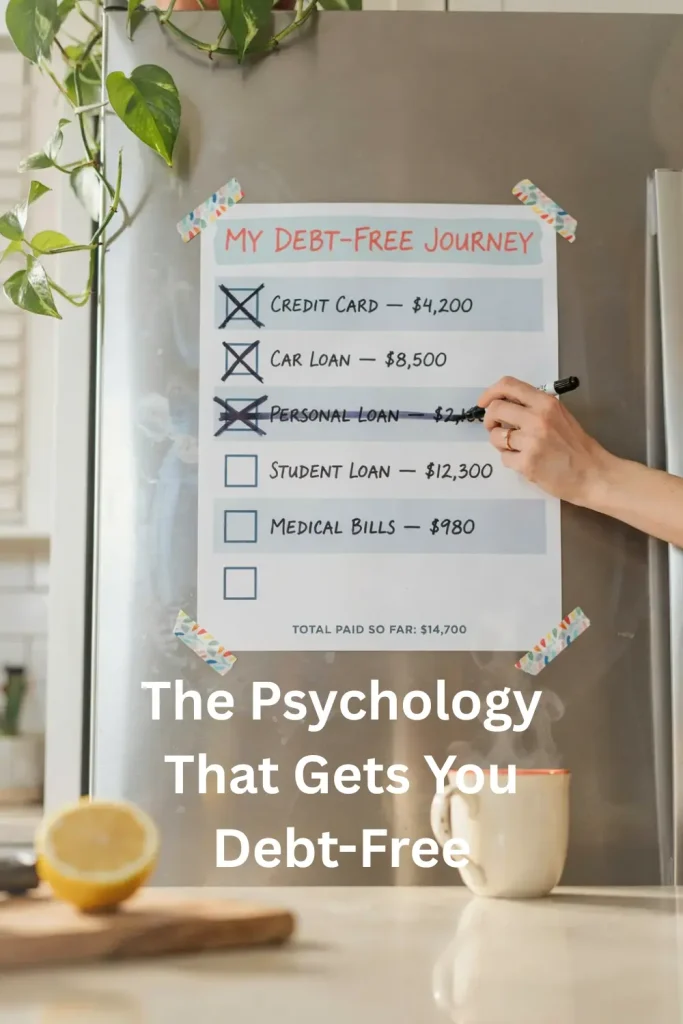

How to Use the Free Printable Debt Snowball Tracker

A tracker turns an invisible process into something you can touch. Print the debt snowball tracker, list your debts smallest to largest in the left column, and write each starting balance at the top of its progress bar. Every payment you make, color in the matching segment. Tape it somewhere you’ll see daily: the fridge, the bathroom mirror, or inside the front door.

The coloring matters more than it sounds. Digital balances update silently in an app you avoid opening. A paper tracker confronts you, in a good way, every time you pass it. Households where both partners see the tracker daily also fight less about money, because progress is shared and visible instead of buried in one person’s banking app.

Make tracker updates a tiny ritual. Same day each month, color the new segment, write the new snowball payment amount, and say the remaining total out loud. It takes four minutes. If you have kids, let them do the coloring. Debt payoff becomes a family project instead of a private stress.

How to Stay Motivated When the Middle Gets Boring

Every debt payoff plan has a dead zone. The first win is behind you, the finish line is a year away, and months four through twelve feel like walking on a treadmill. Expect this. The dead zone is where most plans die, and knowing it’s coming is half the defense.

Build small celebrations into the plan, with rules. Every closed account earns a reward that costs less than $25: a takeout dinner, a movie night, or a plant. It sounds counterproductive to spend while paying off debt, but a $20 reward protecting a $400 monthly habit is the best money in your budget. Just decide the reward before the payoff, so it doesn’t inflate in the moment.

Track milestones beyond closed accounts, too. Crossing under $10,000 total. Hitting 50% paid. Your snowball payment is passing $500. And tell one person what you’re doing, someone who’ll ask how it’s going. Quiet plans are easy to quit. Witnessed plans aren’t. If a month goes sideways and you only manage minimums, that’s a paused plan, not a failed one. Resume next month.

Hit a motivation slump? A no-spend month is the fastest mid-plan booster, and every dollar it frees goes straight into your snowball.

What to Do the Day You Become Debt-Free

Plan the ending before you get there, because the ending is dangerous. The day your last debt dies, your budget suddenly has a huge hole where the snowball payment used to be. For the example above, that’s $675 a month with no assigned job. Money without a job drifts back into lifestyle within two or three months, and old habits follow it.

Give that payment a new job the same week. The standard order works for most people: first, grow your starter emergency fund into a full one covering three to six months of expenses. Then point the rest at retirement contributions and your next big goal, whether that’s a house down payment or a paid-in-cash car.

Keep one or two of the paid-off credit cards open with a small recurring charge on autopay, like a streaming subscription, paid in full monthly. Closed accounts can ding your credit score by shortening your credit history. Used-but-paid accounts rebuild it.

Park that freed-up payment somewhere it earns: compare the best high-yield savings accounts before it drifts back into everyday spending.

Common Mistakes to Avoid

Mistake 1: Skipping the starter emergency fund

Without $500 to $1,000 in cash first, every surprise expense lands on a credit card and erases weeks of progress. Build the small cushion before the first extra payment. It feels slower. It’s actually faster.

Mistake 2: Paying extra on several debts at once

Spreading $250 across five debts means five balances shrink invisibly and nothing ever closes. The snowball’s power is concentration. One target at a time, minimums on the rest.

Mistake 3: Reordering the list by interest rate “just a little.”

Half-snowball, half-avalanche lists usually push the first win months away, which kills the early momentum the method depends on. If you want an avalanche, run a true avalanche. Don’t blend by feel.

Mistake 4: Keeping the paid-off card in your wallet

A zero balance on a card you still carry is an invitation. Take paid cards out of your wallet and delete them from online checkout pages. Out of reach beats willpower every time.

Mistake 5: Sending extra payments “when there’s money left over.”

There is never money left over. Pay the snowball the day after payday, automatically if your bank allows it, and let the rest of the month work with what remains.

Mistake 6: Ignoring windfalls

Tax refunds, bonuses, and birthday money feel like fun money, so they get spent. A single $1,200 refund can erase your second debt. Decide right now that windfalls feed the snowball.

Mistake 7: Quitting after one bad month

A car repair eats your extra payment, you cover minimums only, and the shame spiral says the plan failed. It didn’t. One minimum-only month delays a 26-month plan by a few weeks. Resume and move on.

Mistake 8: Not tracking progress anywhere visible

Progress you can’t see doesn’t motivate. An app you never open is the same as no tracker. Print the chart, put it where you live, and color it monthly.

Quick Start Checklist

- Pull your free credit report at AnnualCreditReport.com to catch every debt (15 minutes)

- Write down each debt’s name, balance, minimum payment, and due date on one page (20 minutes)

- Sort the list from smallest balance to largest, ignoring interest rates (5 minutes)

- Confirm you have a $500 to $1,000 starter emergency fund, or make that goal number one (5 minutes)

- Set every minimum payment to autopay (30 minutes)

- Find your extra payment amount: cancel one subscription and get one new insurance quote today (30 minutes)

- Schedule your extra payment for the day after payday (10 minutes)

- Print the debt snowball tracker and fill in your starting balances (10 minutes)

- Tape the tracker somewhere you’ll see it every day (2 minutes)

- Pick your sub-$25 reward for the first payoff and write it on the tracker (2 minutes)

- Tell one person about your plan and your first target date (5 minutes)

Frequently Asked Questions

Does the debt snowball method really work?

Yes, and the evidence is behavioral, not mathematical. Research published by the Harvard Business Review and studies of real borrowers found that people who concentrate payments on one small debt at a time are more likely to eliminate their full debt than people who spread payments evenly. The method works because completed payoffs keep you motivated enough to finish a multi-year plan.

Should I include my mortgage in the debt snowball?

No. The snowball is for consumer debt: credit cards, car loans, personal loans, medical bills, and similar balances. Mortgages are long-term, lower-rate, and tied to an appreciating asset. Most people tackle the mortgage, if at all, only after consumer debt is gone and retirement savings are on track.

How long does the debt snowball method take?

Most households following it consistently finish in 18 to 36 months, depending on total debt and how much extra they can pay monthly. A $13,000 debt load with $250 extra per month clears in roughly 26 months. Add windfalls like tax refunds, and the timeline shrinks further.

What if I can’t afford anything beyond minimum payments?

Start the snowball anyway with $10 or $25 extra. Tiny extra payments still close small debts and free up their minimums, which becomes your extra payment. At the same time, work the income side: sell unused items, pick up one weekend shift. If minimums themselves are unaffordable, contact a nonprofit credit counseling agency before missing payments.

Is the debt snowball or avalanche better for credit scores?

They affect credit similarly. Both lower your credit utilization as balances fall, which helps your score. The snowball closes accounts sooner, so keep paid-off credit cards open with zero balance where possible. Your score benefits most from on-time payments and falling utilization, which both methods deliver.

Should I stop investing while doing the debt snowball?

It depends on the match. If your employer matches 401(k) contributions, keep contributing enough to get the full match. That’s an instant 50% to 100% return, no debt rate beats. Beyond the match, many people pause extra investing until high-rate consumer debt is gone, then redirect the full snowball payment into investments.

Can I do the debt snowball with a partner who isn’t on board?

It’s much harder but not impossible. Start with your own discretionary spending and any debts in your name. Then share the tracker, not a lecture. Visible progress persuades better than arguments. A monthly 20-minute money check-in with zero blame is the gentlest way to turn a skeptical partner into a teammate.

Your First Debt Could Be Gone by Fall

The debt snowball method isn’t clever math. It’s a motivation machine: smallest debt first, minimums on the rest, every spare dollar on one target, and each closed account makes the next payment bigger. That’s the entire system.

Remember the three things that protect the plan. Build the $500 to $1,000 starter cushion first, so surprises don’t land on a card. Automate the minimums and pay your snowball the day after payday, because leftover money is a myth. And track progress somewhere you can see it, because visible wins are what carry you through the boring middle months.

You don’t need to overhaul your whole life today. You need 20 minutes and one sheet of paper. List your debts from smallest to largest, print the tracker, and schedule one extra payment toward the debt at the top. That $400 store card or that lingering medical bill could be completely gone before fall, and the version of you who closes that first account will not want to stop.

Two years from now, you’ll either have the same balances or a colored-in tracker on the fridge. Start the list tonight.

Sarah Whitman is the Lead Editor at Keenpocket, where she oversees content standards and reviews every published article for accuracy and clarity. With over six years of experience writing about personal finance, Sarah focuses on practical money advice that works for everyday people — covering budgeting, saving strategies, side hustles, debt management, and beginner investing. She believes good financial advice should be honest, actionable, and useful in real life, not just textbook scenarios.